A common scenario encountered quite frequently is individuals adding their children to their home’s title prior to death as a joint tenant with rights of survivorship (JTWROS) as a means to avoid probate. While there are logical reasons why doing so may be a good idea, in general, without proper tax and legal guidance, it can backfire for several reasons.

State property laws establish the value transferred.

Primary responsibility for property law rests with the states and not the federal government; therefore, in order to determine ownership and value the transfer of ownership, one must look to the state’s property laws and something called severability.

Severability is the ability of a joint tenant to unilaterally sever their interest in a jointly held property, and terminate the joint tenancy, which converts the interest to a tenancy in common (TIC) without the need to consult their other owners. Tenancy in common is a form of co-ownership where each tenant holds an individual, undivided interest in the property with no right of survivorship. Each tenant’s interest can be bequeathed or transferred independently.

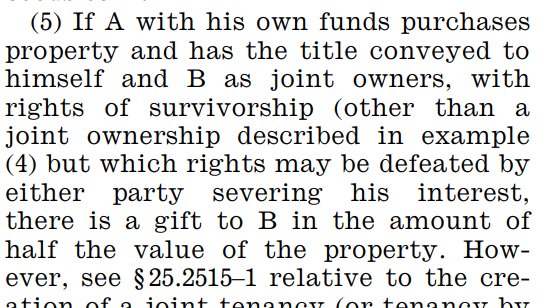

If one lives in a state where severability exists, then the value at the time of title transfer is an equal split. For example, if you add your son and daughters to title, and your home is valued at $600,000, each of you have a $200,000 interest. If you live in a state where severability does not exist, the arrangement is typically treated as though there is a retention of the right to use and benefit from the property for the individual adding their children to the title, because you cannot be unilaterally ousted by the other joint tenants. This is similar to a life interest, and because of that, a more complex calculation needs to take place in determining the valuation of the interest transferred and retained.

Treas. Reg. §25.2512–5(d)(2)

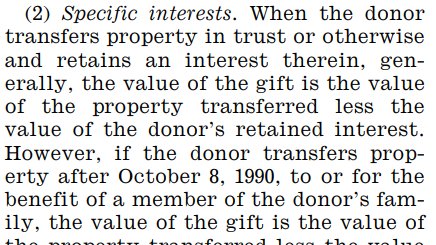

It is considered a federally taxable gift, and a gift tax return should be filed.

As we have established above, in most cases you are transferring value to them, and if that valuation is over the annual gift tax limitations, you have a gift tax return filing requirement for the year in which you made the transfer.

Treas. Reg. § 25.2511-1(h)(5)

Your child’s creditors may come for your property.

By adding another party to title in some states, you may open up the property to more creditors who may have a claim against your child currently or in the future. You may find out, through a divorce proceeding, a tax issue, or a creditor issue, that creditors have a claim to your house. In some cases, creditors can foreclose on the home and have the right to receive the child’s fractional share.

You are giving up a portion of your primary residence capital gains exclusion.

Selling your home, after adding your child to title, means that you can only utilize your primary residence capital gains exclusion of $250k (single) or $500k (married) on your fractional share of ownership. And upon sale of your residence, each child could end up having a long-term capital gains tax bill if the home is not their primary residence.

Full Step-Up in Basis Still Possible When Adding Individuals to Title—But Often Missed by Tax Practitioners

Adding individuals to a property title can still allow for a full step-up in basis at death, though it’s frequently overlooked. According to IRC 1014 (income tax code) , the basis of inherited property is its fair market value at the decedent’s death, provided it wasn’t sold or otherwise disposed of before then. Under estate tax laws, IRC 2036 (estate tax code) includes property in the gross estate if the decedent retained the right to use it. This inclusion triggers IRC 1014’s step-up in basis.

Moreover, IRC 2040 (estate tax code) stipulates that the gross estate includes the value of property held as joint tenants with right of survivorship, unless the other joint tenant can prove they originally owned the property. Without adequate consideration for adding someone to the title, 100% of the property’s value is included in the gross estate. However, in practice using our example above, only a proportional share (e.g., one-third) often receives the step-up in basis. The interplay between the assets being included for estate tax inclusion is often missed, but a critical issue for determining the correct basis for income tax purposes.

Aligning Heirs and Understanding Tax Implications Before Title Changes

In summary, maybe adding individuals to title can serve your tax needs, but other issues such as family dynamics can influence a lot of things that make this an unideal scenario. To ensure that you and your heirs achieve optimal outcomes and prevent unexpected issues, it’s critical to keep everyone informed and include them in tax discussions with your tax professional, as well as in legal discussions about property ownership and inheritance with your legal advisors.