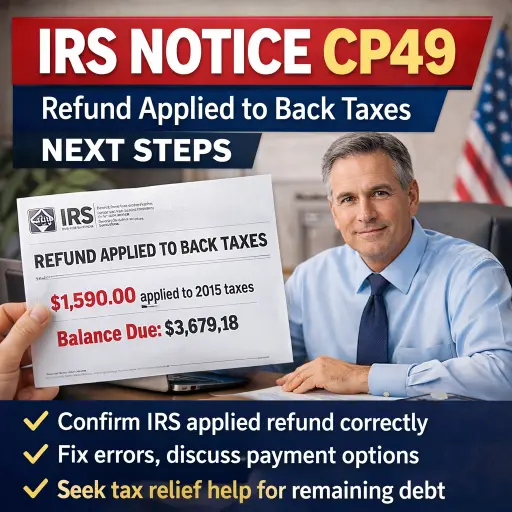

IRS Notice CP49 is the letter the IRS sends when it uses some or all of your current-year refund to pay a past-due tax balance from another year. In plain English: you expected a refund, but the IRS redirected it to an older bill.

For many taxpayers, CP49 is confusing because it doesn’t feel like a typical “you owe” notice at first—it feels like the IRS changed your refund. And that’s essentially what happened. The key is figuring out whether the IRS applied the refund to the correct tax year and balance, and then deciding what to do about any remaining debt.

If you’re worried you’ll “get in trouble” for receiving CP49, take a breath. This notice is often informational—but it is also a signal that there’s an unresolved IRS balance that deserves a plan.

IRS Notice CP49 At a Glance

| Item | What it means |

|---|---|

| Notice type | Overpayment application (refund applied to another year) |

| Common trigger | You filed a return showing a refund while an older balance exists |

| What it tells you | How much of your refund was applied, and what (if anything) remains due |

| Followed by | Often nothing immediate—unless a balance remains and the account is in collections |

| Recommended action | Confirm accuracy, then resolve the remaining tax debt |

IRS Notice CP49 Explained, Part by Part

CP49 layouts can vary, but most include these same components.

Part 1: Refund application summary on IRS Notice CP49

Near the top, CP49 typically shows two critical numbers:

- How much refund (overpayment) was applied from the return you just filed

- What balance remains for the year the IRS applied it to (if any)

This is where you confirm whether the IRS applied the refund to the year you expected—and whether the remaining balance makes sense.

Part 2: Payment voucher or coupon

CP49 often includes a detachable payment section. It’s there for taxpayers who want to mail in a payment toward any remaining balance. Even if you don’t plan to mail a check, this section is useful because it usually repeats identifying details like the tax year and amount.

Part 3: “What you should do now”

The IRS usually tells you to pay the remaining amount due. CP49 may also include reminders for special circumstances, such as:

- If you’re currently in a hardship/collection pause and your finances haven’t changed, the notice may not require immediate action beyond keeping records.

- If you’re in bankruptcy, CP49 can be informational due to bankruptcy protections, and the right next step depends on your case.

If you disagree with the application or the balance, CP49 also points you to IRS contact options so you can request a review.

Part 4: Payment and resolution options on IRS Notice CP49

This section often explains that if you can’t pay the full remaining balance, you may be able to pursue alternatives, such as:

- Monthly payment arrangements

- Settlement options (in limited cases)

- Temporary collection relief if paying would create serious hardship

Not every option fits every taxpayer, but CP49 is your cue to evaluate what’s realistic.

Part 5: If the IRS doesn’t hear from you regarding IRS Notice CP49

CP49 typically warns that interest and penalties can continue on any remaining unpaid balance. That’s why it’s important to act—even if your first step is simply verifying the numbers.

Part 6: Extra details and recordkeeping reminders for IRS Notice CP49

Toward the end, CP49 often includes general “where to find forms,” “how to pay,” and “keep this for your records” type information. Don’t skip it entirely, but focus first on the numbers and the year(s) involved.

When the IRS Sends Notice CP49

The most common CP49 scenario looks like this:

- You file a tax return that shows a refund.

- The IRS sees you have an unpaid balance from a prior tax year (or years).

- The IRS applies all or part of your refund to that older balance.

- The IRS sends CP49 to explain what it did.

CP49 can also show up when the IRS posts a balance after processing—sometimes due to penalties, interest, or an adjustment—then uses a later refund to cover it.

What You Should Do If You Receive CP49

Step 1: Verify the IRS applied your refund correctly

Before you assume the IRS did it right, confirm:

- The refund amount matches your filed return

- The year the refund was applied to matches your records

- The remaining balance (if shown) matches prior notices, transcripts, or your payment history

- Any payments you already made are reflected correctly

This step matters because a misapplied payment or incorrect balance can follow you for years if it isn’t corrected.

Step 2: Fix errors fast if something doesn’t add up

If you believe the IRS applied the refund to the wrong year, missed a payment, or overstated the balance, your next move is to request a review using the contact details shown on the notice.

Practical tip: Keep copies of canceled checks, bank confirmations, e-file acceptance pages, and any prior IRS letters. Clear documentation shortens the back-and-forth.

Step 3: Evaluate penalty relief for the older balance

CP49 is about the refund application—but it often points to a bigger issue: the underlying debt may include penalties you could potentially reduce.

Depending on your situation, it may be worth exploring penalty relief strategies such as reasonable cause or administrative relief. Penalty relief isn’t automatic and shouldn’t be assumed, but when penalties are a large part of the balance, it’s often worth a careful review.

Step 4: Choose the best path to resolve the remaining tax debt

Once you confirm the numbers, you have options:

- Pay the remaining balance in full if you can (fastest way to stop additional accruals)

- Set up a payment plan if you need time

- Request temporary collection relief if paying now would create a genuine hardship

- Explore settlement options when appropriate (these are highly fact-specific and not available to everyone)

The best approach depends on income, expenses, assets, and how stable your cash flow is.

Can You Get Your Refund Back? Offset Bypass Refund (OBR) for Hardship Situations

If you received IRS Notice CP49, the IRS is telling you it applied your refund to an older tax debt. For many people, that offset is already complete for the return that triggered the notice.

However, there may be a future-looking strategy worth discussing if you expect a refund again and you’re facing a genuine financial crunch: an Offset Bypass Refund (OBR). In certain hardship situations, an OBR request asks the IRS to release a refund instead of automatically applying it to back taxes.

What an OBR is (in plain English)

An OBR is a hardship-based request. It’s designed for taxpayers who can show that losing the refund would create serious financial strain—for example, difficulty covering essential living expenses. It’s not a loophole and it’s not guaranteed. It’s a narrow option that depends on facts, documentation, and timing.

Why timing matters with refund offsets

CP49 is often the “after” picture—your refund has already been redirected. OBR planning is often about the “before” picture: preparing early enough (and cleanly enough) so a future refund has a chance to be released when hardship is documented.

Why this is where a CPA firm’s long-term approach beats a “tax relief” company

Most tax resolution firms are built to handle a single notice and move on. OBR, when it’s even an option, usually requires a coordinated approach across multiple moving parts:

- Correct, timely filing so the refund exists and processes normally

- Clean records so the IRS account history supports what you’re requesting

- Hardship documentation that is specific and organized (not vague)

- Follow-through to monitor what the IRS posts, applies, and releases

That kind of work is much easier—and more effective—when you have a CPA firm that stays with you year after year. Corridor Consulting CPAs supports clients beyond the immediate notice: we help stabilize compliance, improve planning, and coordinate the resolution strategy so you’re not stuck repeating the same refund-offset cycle every tax season.

What Corridor Consulting CPAs does differently

If OBR is worth exploring, we help clients take a structured path:

- Assess eligibility and constraints based on your IRS account and financial reality

- Prepare a clear hardship narrative backed by numbers (income, expenses, and supporting documents)

- Coordinate your tax filing and resolution plan so the refund, the debt, and your compliance all line up

- Stay involved long-term to reduce repeat offsets by addressing the underlying tax debt and improving future tax planning

Important note: OBR is fact-specific and timing-sensitive. The right first step is a professional review of your CP49, your IRS account history, and your current financial picture so you know what options are realistic.

Why Work With a CPA Firm, Not Just a Tax Relief Company

Refund-application notices like CP49 can seem simple—until you discover the underlying balance involves multiple years, missing payments, penalties, or old filing issues.

A CPA firm can help by:

- Confirming the IRS applied the refund correctly (and proving it if they didn’t)

- Reviewing transcripts and posting history to identify errors

- Building a resolution plan that fits your finances and your tax filing strategy

- Helping you stay compliant going forward so refunds aren’t repeatedly intercepted

Corridor Consulting CPAs is a licensed CPA firm—built for both tax resolution and ongoing tax/accounting support—so you’re not stuck bouncing between a “relief” company and a separate compliance provider.

How Corridor Consulting CPAs Can Help With CP49

For taxpayers in Cedar Rapids, across Eastern Iowa, and nationwide, we can help you:

- Validate whether CP49 was applied correctly and to the right year

- Identify what’s driving the balance (tax, penalties, interest, posting issues)

- Communicate with the IRS and track the account until it’s resolved

- Pursue penalty relief where appropriate

- Set up a sustainable resolution plan—payment plan, hardship pathway, or other supported option

Take the First Step Toward IRS Tax Relief

If CP49 surprised you, you’re not alone. The most important thing is to avoid guessing. Verify the numbers, confirm the year the refund was applied to, and put a plan in place for any remaining balance.

Corridor Consulting CPAs can help you move from confusion to clarity—with professional support that prioritizes accuracy, transparency, and long-term stability.

CP49 FAQs

Can CP49 still mean I’ll get a refund?

Yes. If your refund is larger than the past-due balance the IRS applied it to, CP49 typically shows both:

- The amount the IRS applied to the older year, and

- The remaining amount you should receive (usually by check or direct deposit, depending on your return settings).

Example:

If your refund is $1,500 and your prior-year balance is $1,000, the IRS may apply $1,000 and you may still receive $500.

Does CP49 mean I’m being audited?

Usually, no. CP49 is most commonly about a refund being applied to an existing balance—not an audit. That said, if the balance came from an adjustment, it’s worth understanding why.

Should I ignore CP49 if the IRS already took the refund?

Don’t ignore it. Even if the refund was applied, you still need to confirm the application is correct and determine whether a balance remains that needs a plan.